The Department for Work and Pensions’ Spring Forecast 2026 is, on one level, exactly what these documents often are: a dense set of tables, assumptions and projected expenditure lines. But behind the spreadsheets sits a much bigger story. This is not simply a forecast of welfare spending rising over time. It is a warning that the structure of the welfare state is changing, and changing quickly.

The headline numbers are large enough to command attention on their own. Total UK welfare spending is projected to rise from £310.3 billion in 2025/26 to £374.3 billion by 2030/31. The State Pension remains the single largest item, increasing from £136.4 billion to £180.4 billion across the same period. But the most important development is elsewhere. The part of the system growing fastest is not traditional unemployment support, nor one-off cost of living interventions. It is health and disability related spending, especially Personal Independence Payment and incapacity related support within Universal Credit.

That matters because it tells us something fundamental about the pressures now being carried by the welfare system. For many years, debate about welfare was often framed around work incentives, conditionality and short-term income replacement. The Spring Forecast points to a different reality. The system is increasingly being asked to respond to long-term ill health, disability, mental health needs, housing pressures and reduced capacity to participate fully in the labour market. In other words, welfare is becoming less about temporary disruption and more about sustained structural support.

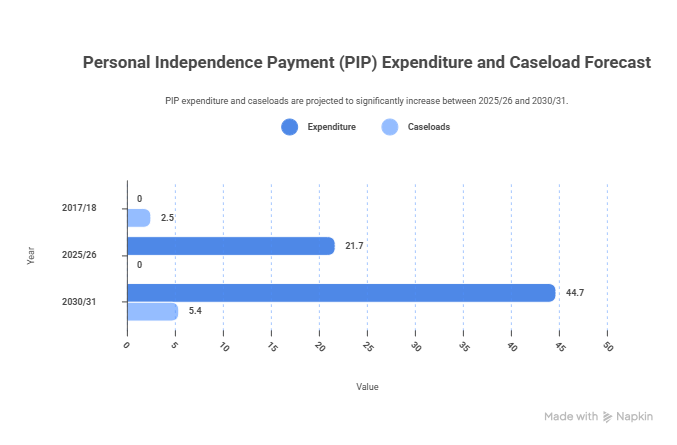

The clearest example is Personal Independence Payment. The forecast shows PIP expenditure rising from £21.7 billion in 2025/26 to £44.7 billion by 2030/31. That is a remarkable increase in a relatively short period. Caseloads are forecast to rise from 2.5 million in 2017/18 to 5.4 million by 2030/31. Even allowing for population growth, changing awareness, improved diagnosis and greater take-up, that is not normal system drift. It is a sign of deep and persistent demand growth.

Attendance Allowance also rises materially, from £7.7 billion to £11.1 billion. This reflects the ageing population, but it also reinforces a broader point. Spending pressures are building at both ends of the age profile. Pensioners remain a major and expanding part of total spend, but working-age ill health is growing so fast that the old distinction between pensioner support being the dominant long-term pressure and working-age support being more cyclical no longer feels secure.

Indeed, one of the most important trends in the forecast is the changing relationship between pensioner spending and spending on working-age adults and children. Historically, pensioner spending has tended to dominate. The forecast suggests that by 2029/30, spending on working-age people and children overtakes pensioner spending. That is a profound structural shift. It should force policymakers to ask whether the welfare state we have is still designed for the welfare pressures we now face.

Much of this rests on the interaction between health, disability and Universal Credit. Expenditure on incapacity related benefits, including the Universal Credit health element, is forecast to exceed £91 billion by 2029/30. That figure alone should end any lingering idea that the main challenge in welfare is purely one of short-term unemployment. The system is increasingly supporting people whose barriers to work are not brief interruptions but serious and sometimes enduring health conditions. Some of this may reflect deteriorating public health, some the long aftermath of the pandemic, some the growth in recognised mental health conditions, and some the consequence of labour market changes that are less accommodating to people with fluctuating capability. Whatever the cause mix, the trend is persistent and expensive.

This is where the fiscal risk becomes political risk. If the system continues to absorb demand of this scale, governments will be under growing pressure to tighten eligibility, slow caseload growth, reduce award levels or make it harder to access long-term support. Yet each of those measures carries its own risks. Restricting access may reduce projected expenditure in the short term, but it may also shift cost elsewhere: into local authority hardship services, NHS pressures, temporary accommodation, adult social care, debt, homelessness support, and crisis provision. What looks like savings in one department can easily become unmanaged cost in another.

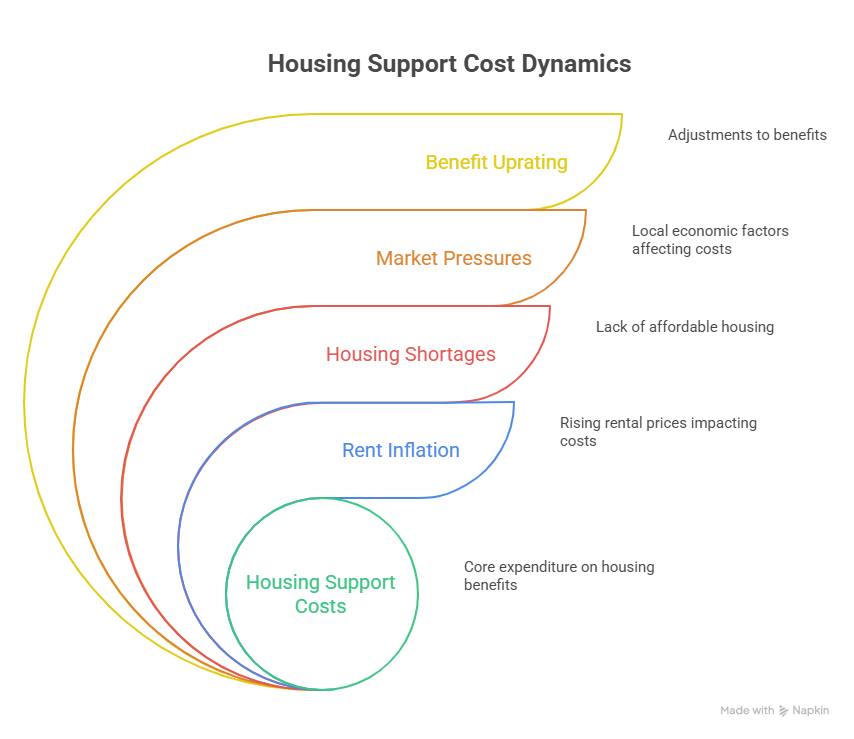

That is particularly true when considering housing support. Combined expenditure on legacy Housing Benefit and the Universal Credit housing element remains substantial and stubborn, sitting at around £25 billion to £30 billion a year across the forecast period. This is less explosive than PIP growth, but no less significant. Housing support remains highly exposed to rent inflation, shortages of affordable housing, and local market pressures. It is a high, stable and deeply embedded cost base. If rents continue to outpace earnings and benefit uprating, pressure will not disappear. It will intensify, particularly in areas already struggling with affordability, temporary accommodation costs and demand for discretionary support.

The forecast also reminds us that not all growth in spending is the same. In nominal terms, welfare spending rises sharply. In real terms, the increase is less dramatic, from £314.5 billion in 2025/26 to £352.5 billion in 2030/31. That distinction matters. Some of the increase is inflation rather than an expansion in underlying generosity. But that should not reassure policymakers too much. Even if part of the spending rise is price related, the real-terms growth is still substantial, and the caseload trends behind it are hard to dismiss as a statistical illusion.

There are, however, reasons to be cautious about treating every projected line in the forecast as fixed truth. The document itself acknowledges important methodological limitations. The breakdown of Universal Credit expenditure into elements such as health, housing and children is based on analytical assumptions, and the DWP openly notes that other credible breakdowns could be reached. That is not a minor technical footnote. It means that even where expenditure is rising clearly, the precise attribution of why it is rising is less certain than some headline readings may imply.

There are similar concerns elsewhere. Historical data has been revised, including the removal of around £2 billion per year of pensioner Housing Benefit from disability and health tables. That correction may improve accuracy, but it is also a reminder that baselines move. If the baseline moves, so too does the narrative. Likewise, caseload overlaps between benefits cannot simply be added together, and some estimates, such as overlap between Universal Credit health and ESA, are experimental. This makes it harder to answer one of the most important strategic questions: how many individual people are being supported, with what mix of needs, and at what combined cost?

There is also an important blind spot around devolved benefits. From 2020/21 onwards, parts of disability related expenditure such as DLA, PIP and Attendance Allowance are shown for England and Wales only, because Scotland has taken on devolved responsibility. That means the UK-wide picture is no longer fully visible in the same way. Funding still exists through the Scottish Government settlement, but the reporting becomes less transparent if one is trying to understand the total burden of disability related support across the whole UK. In practical terms, that creates a data gap in one of the most important areas of long-term spending growth.

The economic assumptions underpinning the forecast are another source of risk. The numbers are aligned to the Office for Budget Responsibility’s March 2026 Economic and Fiscal Outlook. That is standard practice, but it matters greatly. If the OBR’s assumptions on growth, unemployment, earnings or inflation prove wrong, then welfare spending will move with them. A weaker economy would push up Universal Credit and related supports. Sticky inflation would increase uprating pressures. Weak wage growth would worsen the affordability gap for households already dependent on partial support from the system. In short, the forecast is only as robust as the economy beneath it.

So where does this leave us by 2030?

On current trends, by 2030 the welfare state is likely to look more health-led, more disability-led and more structurally embedded than it did a decade earlier. It will still be carrying the cost of an ageing society through the State Pension and Attendance Allowance, but the faster political pressure point will be working-age health. PIP is likely to remain the most contested area of expenditure because its growth is so visible and so difficult to explain away as a short-term anomaly. Universal Credit will remain central, but increasingly not as a pure out-of-work benefit. Instead, it will continue evolving into a broad income platform carrying housing costs, child support and major health-related expenditure within one large and complicated framework.

By 2030, unless there is a major change in health outcomes, labour market accessibility or housing affordability, the debate will probably no longer be whether welfare spending is too high in the abstract. The real argument will be whether the state has built the right institutions around the spending. If the answer is no, the result will be continued fiscal anxiety, repeated attempts at eligibility reform, and growing displacement of unmet need onto councils, health services and families.

There is also a real risk that by 2030 the political language of welfare reform becomes even more detached from the lived reality of claimants. If ministers continue to speak as though rising expenditure is primarily a problem of control, fraud or weak incentives, they will misdiagnose what the forecast is telling them. The dominant growth areas are not random. They point to more people living with complex health conditions, more households struggling with long-term affordability, and more reliance on state support not because people are disengaged, but because the economy and public services are not consistently preventing vulnerability from becoming permanent.

That does not mean every projected increase should simply be accepted without scrutiny. Forecasts can be wrong. Caseload assumptions can be challenged. Eligibility systems should be tested for fairness and consistency. But the deeper lesson of the Spring Forecast is that the welfare state is becoming a mirror of wider social and economic strain. You can try to narrow entitlement, and some governments surely will. But unless the drivers of poor health, insecure housing, low resilience and labour market exclusion are addressed more effectively, the pressure will not vanish. It will simply reappear elsewhere, often in ways that are more expensive and more damaging.

By 2030, the UK is likely to find itself at a fork in the road. One path is a welfare system under permanent fiscal suspicion, repeatedly tightened at the edges while demand continues to rise underneath it. The other is a more honest settlement, where policymakers accept that welfare has become one of the country’s main shock absorbers for demographic change, poor health and housing stress, and start designing policy around that fact rather than arguing with it.

If the Spring Forecast 2026 is read properly, it does not just tell us where money is going. It tells us where the country is under strain. And on present evidence, that strain is becoming more chronic, more health-related and more difficult to contain with old policy assumptions.